Trever Christian and John Schwalbach, Partners

July 5, 2024

Share This:

googleImagine this: As a business owner, you’ve worked for years to build a business, leading your company to new heights. You hold regular meetings, setting ambitious goals while meticulously charting a course for success. Yet, in the midst of rapid growth, persistent questions remain: Will I have enough financial resources to maintain my desired lifestyle after I sell my business? Is my personal financial plan secure?

For business owners, personal financial planning is different. The foundation of your wealth – your business – can be a double-edged sword. It fuels your success, but its illiquidity creates a unique set of challenges. Unlike salaried employees, a significant portion of your net worth is tied up in the company. This makes traditional financial planning less applicable.

Key considerations for a business owners’ personal financial plan

The Freedom Score

A Freedom Score is the financial target you need to achieve, through a business sale or other means, to secure a future that aligns with your values and goals. The Freedom Score isn’t just about retirement; it’s about having the freedom to choose when and how you work.

Achieving true freedom goes beyond a number. It’s about clarity. What if the unexpected happened to your business? Would your personal finances still be okay? Could you still live the life you envision?

Achieving true freedom goes beyond a number. It’s about clarity. What if the unexpected happened to your business? Would your personal finances still be okay? Could you still live the life you envision?

Shared vision in your personal plan

Mutual understanding of financial goals and values provides support and motivation to both you and your spouse. With clarity on your shared vision, you can encourage each other to stick to your long-term plan, make necessary sacrifices along the way, and celebrate milestones together.

The right financial guide

Finding the right guide can elevate the outcomes of your planning. Most wealth management professionals do not possess the specialized expertise to navigate the complexities of business ownership, particularly when it comes to your eventual exit strategy and how that ties into your personal financial plan. That’s why you want to identify a partner who can help you through the full planning process.

An early start to planning

Time is your most valuable asset. Don’t let the demands of running a business push your financial planning to the back burner. Engaging with knowledgeable advisors early is essential. The right team will become your strategic partner – helping you stay organized, bridge the gap between personal and business finances, and handle the multitude of challenges that business owners face.

But where do you begin? This blog post aims to illuminate why financial planning is different for business owners and answer the critical questions to help you sleep soundly at night. We’ll explore the unique challenges you face, from determining your Freedom Score to navigating complex tax situations. We’ll also provide actionable strategies to build a tailored roadmap that brings you closer to your financial goals, both during and after your ownership years.

Here are some of the key questions we’ll address:

- How do I begin planning for my business exit?

- How much do I need to accomplish my financial goals?

- How do I know how much my business is worth?

- How do I close the gap between my current business value and what I need in the future?

- Is my business protected if something goes wrong?

- Will I be able to exit and retire when I want to?

By the end of this post, you’ll have a clearer understanding of the financial planning landscape for business owners and feel empowered to take actionable steps towards achieving your financial goals and values.

Planning For a Successful Exit

An integral first part of personal financial planning for business owners is preparing for the eventual exit from your business. Planning an exit strategy is a critical aspect, and it’s never too early to start. By adopting an “exit-ready” mindset, you enhance your business’s value and ensure its resilience, making it more attractive to potential buyers. This proactive approach involves setting measurable goals, navigating potential challenges, and aligning your business operations with your long-term personal and financial objectives.

Understanding Your “Why”

What is driving your decision to sell? Understanding your motivations—both the “push” factors like stress or health issues and the “pull” factors such as pursuing new passions—is essential. Identifying these factors early ensures that your exit strategy aligns with your long-term personal and financial goals.

A well-executed strategy aims for what can be termed a “Euphoric Exit”. A Euphoric Exit is the culmination of a well-executed exit strategy that not only meets but exceeds your financial and personal expectations. It’s the moment when you step away from your business with complete clarity, knowing that the sale has fulfilled all your objectives—be it financial security, legacy preservation, or personal freedom. Achieving a Euphoric Exit requires extreme clarity on what your ideal exit looks like. This includes having a clear vision of your post-exit life, the financial returns you expect, and the legacy you wish to leave behind.

The Emotional Journey

For many business owners, your company is more than just a source of income—it’s an integral part of your identity. The decision to sell can therefore be a deeply emotional one. Are you ready to step away from the role that has defined you for so long? What will your life look like after the sale? Addressing these questions is vital for ensuring not just a successful exit, but also a fulfilling post-business life.

The Path Forward

Planning for a successful business exit goes beyond the financial transaction—it’s about aligning the sale with your personal goals, ensuring your team’s well-being, and preparing emotionally for the next chapter of your life. By starting the process early and addressing all aspects of the transition, you can ensure a smoother and more rewarding exit. Whether your motivation is pursuing new passions or preserving your business’s legacy, a well-crafted exit plan helps you achieve your long-term goals and secure a fulfilling life post-business

The Freedom Score and Your Personal Financial Plan

What if your business is the key to a future brimming with freedom and financial security? This is the power of your Freedom Score. The Freedom Score is the financial target you, as a business owner, need to achieve to secure a future that aligns with your values and goals. It’s about living life on your own terms, free from the unpredictability of markets or the demands of your work.

How to calculate your Freedom Score

The Freedom Score is a essential part of business owners’ personal financial plan, and to calculate your score requires a look at four main components:

- Desired Lifestyle: Define your ideal future lifestyle in as much detail as possible. This includes mapping out travel plans, hobbies, volunteer activities and who you want to spend your time with.

- Annual Income and Expenses: Calculate your estimated annual expenses and the income you will need to generate to maintain your desired lifestyle.

- Investment Returns: Factor in the projected rate of return on your current investments along with investments that will materialize in the future, such as when you sell the business or savings that will go into investment accounts while running your business.

- Business Value: Understand your business’s current market value along with a reasonable forward looking growth rate. Because your business likely contributes heavily to your Freedom Score, you want to have an accurate, up-to-date valuation. If you underestimate the value of your business, you may work longer than is necessary. Likewise, if you overestimate the value of your business, you may sell your business too soon and risk not having the resources to live your desired lifestyle.

Your business and the Freedom Score

The Freedom Score evaluates your financial readiness to fund the next phase of your life after the sale of your business. It is meant to measure the degree to which you are dependent on your business as an asset to meet your retirement goals. The Freedom Score also helps calculate your Freedom Point – the projected year when the sale of your company will generate enough to fund your desired lifestyle for the rest of your life.

But what happens if your current business value falls short of funding your desired lifestyle? This situation is known as the value gap. Understanding the importance of early exit planning can help you close this gap and maximize the value of your business when the time comes to sell.

How business owners incorporate the Value Gap into their personal financial planning

Let’s evaluate the scenario where the current value of your company isn’t enough to fund future goals. The gap between the business’s current worth and the Freedom Score is what we call the Value Gap. If you have a Value Gap in your personal financial plan, you have options. Many strategies can help bridge this gap and unlock your own path to freedom.

Closing the Value Gap

Identifying a value gap isn’t a dead end; it’s a roadmap for strategic improvements. Here’s where a financial planner becomes your partner:

- Business Growth Strategies: Planners that specialize in business value acceleration can work with you to develop strategies to increase your business’s value. This could involve expanding your customer base, developing a new product line, improving profitability, or streamlining operations. By growing your business’s value, you can decrease the size of your value gap.

- Investment Planning: Your advisor can help you optimize your investment portfolio by creating plans to help you achieve your savings and return goals.This additional wealth can help bridge the gap between your business value and your Freedom Score.

- Lifestyle Planning: They can also help you refine your desired lifestyle. Perhaps there are areas where you can make spending adjustments without sacrificing your most important financial goals and values. This reduction in your annual expenses can help shrink the value gap.

By working together on these strategies, you can close the value gap and achieve your Freedom Score. Remember, a healthy value gap analysis isn’t just about the numbers – it’s about aligning your financial resources with the life you envision for yourself.

Business valuation and your personal financial planning

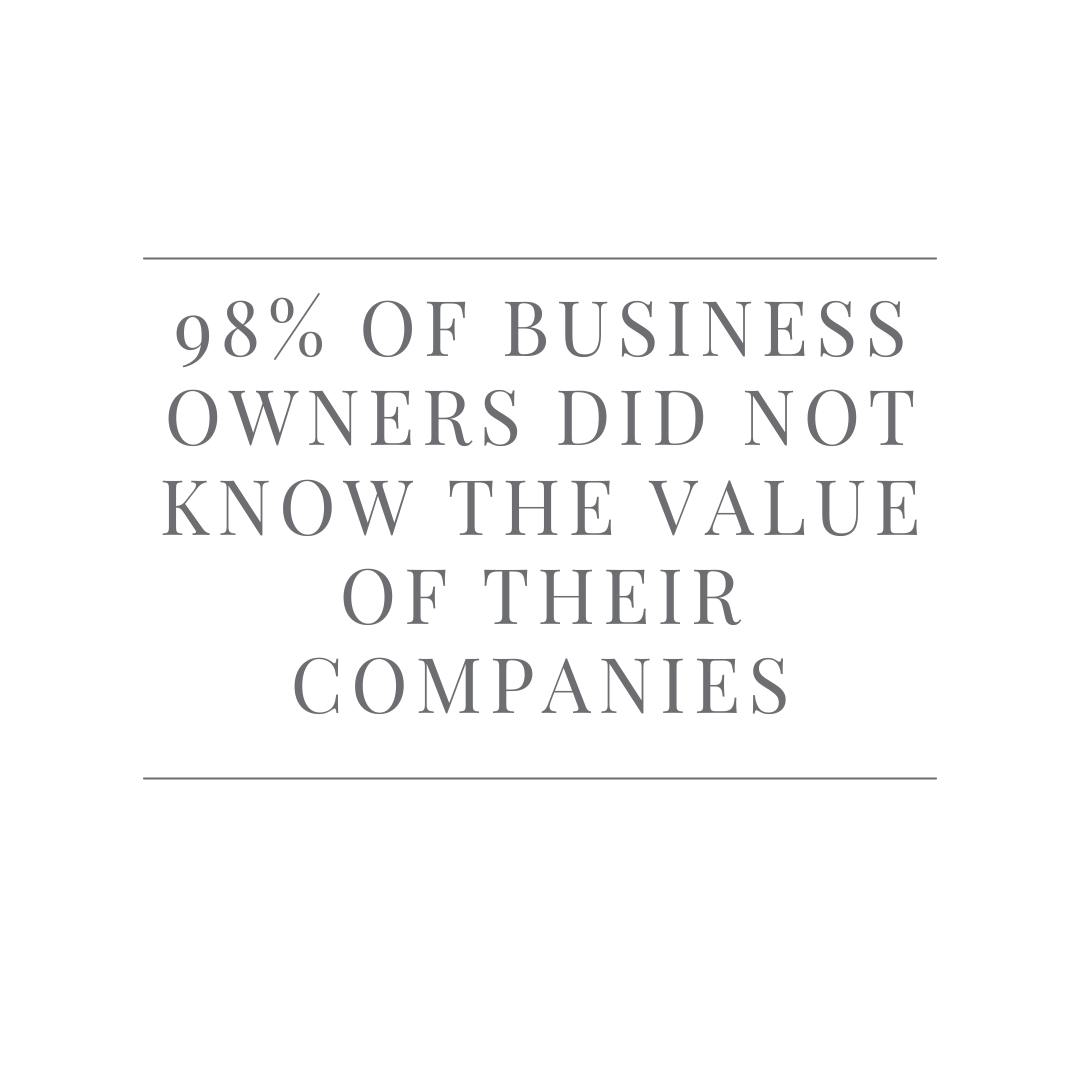

A significant portion of a business owner’s net worth—often between 50-90%—is typically tied up in their business. Knowing the true value of such a substantial asset is crucial. Surprisingly, in a 2022 survey conducted by M&T bank, 98% of business owners did not know the value of their companies. Many rely on guesswork, like industry averages, which can miss the mark entirely.

Why your business valuation in critical in your financial plan

- Informed Decisions: A valuation is not just about knowing a dollar figure; it’s about gaining valuable insights to fuel strategic decision-making. A professional valuation provides a clear picture of your business’s health, informing choices for growth initiatives, potential acquisitions that complement your existing operations, and crafting a well-defined succession or exit plan. This empowers you to maximize your business’s value and achieve your long-term personal financial planning goals.

- Bridging the Heart/Head Gap: Often, an owner’s emotional attachment (the “heart”) can cloud their judgment of the business’s fair market value (the “head”). Valuation helps bridge this gap and ensure the business is accurately reflected on the balance sheet.

- Planning for the Future: What if you sold your business today, versus next year versus five or 10 years from now? An accurate business valuation empowers you with powerful “what-if” scenarios for informed future planning.

- Risk Mitigation: A key risk management tool is a buy-sell agreement that includes a professional valuation. This agreement sets a fair market price for ownership transitions, minimizing disputes and ensuring a smooth handover. This protects your business and your financial well-being.

Business Valuation Made Easy

Gone are the days of expensive, time-consuming business valuations. At Freedom Financial Partners, we use a tool called BizEquity to offer a faster, more affordable way for our business owner clients to get an annual valuation report. In seven quick steps, BizEquity provides actionable insights that benchmark your business versus industry peers and allow for ongoing updates as your business grows and evolves.

Beyond the business sale: understanding True Net Proceeds

Many business owners mistakenly equate the gross sale price with their personal financial gain from a sale. Selling costs like broker commissions, taxes, accounting costs, legal fees, and potential key employee bonuses significantly impact the net proceeds you receive. Factoring these costs into your personal plan is crucial for understanding the real financial outcome.

Transitioning Your Personal Finances

As you move towards a successful business exit, you will need to reallocate personal expenses that currently run through your business to your personal budget. This ensures your financial plan accurately reflects your future outflows. Here are some common examples:

- Phone and internet

- Travel and entertainment

- Health insurance

- Office space rent

- Equipment and supplies

- Retirement plan contributions

Elements of a business owner’s personal financial plan

As a business owner, your financial future hinges on more than just the success of your business. Achieving your Freedom Score—a clear financial target that ensures you can live the life you envision—requires a thorough understanding of your business’s value and how it integrates into your overall financial plan.

Early and comprehensive financial planning is essential. By addressing all elements of your personal financial plan now, you can secure your future, mitigate risks, and create a roadmap that aligns with your goals and values. We will introduce some key areas and concepts below that every business owner should consider when thinking through a comprehensive financial personal plan.

Wealth management/investments

A key component of effective investment planning is understanding exactly what you are retiring to. This vision will guide how you structure your investments to replace the income your business once generated, ensuring that your financial resources adequately support your new lifestyle.

As you transition from being a business owner to owning a significant investment portfolio post-sale, it’s crucial to recognize that the skills which made you successful in business may not directly translate to success as an investor. Whereas entrepreneurship often rewards risk-taking and quick decision-making, successful investing often requires a different set of virtues: patience, diversification, and a well-measured approach to risk management. Warren Buffet summed this up best when he said, “Becoming wealthy is hard, but staying wealthy is harder.” ”

Investing for your personal plan

Investment strategies should be aligned closely with your individual financial goals. This alignment ensures that your investment decisions support your overall financial plan, rather than mirroring the strategies of friends or peers whose financial situation, risk profile and objectives might differ significantly from yours. It’s important to invest based on what’s best for your unique circumstances, not by following the latest trends or the investment choices of others.

Power of diversification

For many business owners, their business is not just a source of income; it represents the bulk of their wealth. Estimates suggest that a business can comprise between 50 to 90% of a typical business owner’s total net worth. This concentration in a single asset class, while often profitable, exposes owners to significant financial risk. The sooner a business owner can “take money off the table” from the business to invest in other asset classes, such as stocks, bonds and real estate, the more secure their financial future will likely be.

Diversification with investment portfolios

Imagine your investment portfolio as a sturdy bridge. Diversification is like the multiple support beams holding it up. By spreading your investments across different asset classes (stocks, bonds, real estate), industries, and geographic regions, you create a more resilient structure. This planning and investing approach helps mitigate potential losses if a single investment or industry sector experiences a downturn. Think of diversification as a safety net – if one area weakens, the others can help keep your portfolio stable.

While stocks and bonds are core holdings, consider incorporating alternative investments to further diversify and potentially hedge against inflation or market volatility. Global Exposure is also crucial; don’t limit yourself to your domestic market. Investing in international stocks and bonds can provide exposure to different economic cycles and growth opportunities, potentially enhancing returns and mitigating risk. Additionally, within the stock market, diversify by company size (large-cap, mid-cap, small-cap) and industry sector (technology, healthcare, consumer staples) to avoid overexposure to any one company or sector’s performance. By implementing these diversification strategies, you create a more resilient portfolio less susceptible to market fluctuations.

Risk Management for a Less Volatile Investment Future

While diversification is the foundation of a secure portfolio, it’s not the only safeguard. Just like a bridge needs constant monitoring and maintenance, your investments require a proactive approach to risk management. This involves identifying potential threats, such as market volatility or inflation, and implementing strategies to minimize their impact.

Risk management involves finding the right balance between risk and return. The optimal portfolio is a mix of assets that maximizes return for a given level of risk. By employing risk management strategies, you can achieve the highest possible return while maintaining an acceptable risk.

By focusing on these principles, you can develop an investment strategy that not only preserves but also grows your wealth, ensuring that your post-business years are as rewarding and secure as the years you spent building your business.

Business and Personal Insurance Planning

As a business owner, safeguarding your financial future extends beyond the walls of your company. A comprehensive insurance plan protects not only your personal assets but also your business interests. This strategic planning provides peace of mind as you transition from active management to retirement and ensures the well-being of your loved ones and your business legacy.

Insurance Coverage in a Business Owner’s Financial Plan

Life Insurance

Life insurance plays a pivotal role, especially for business owners. It can provide the necessary funds for your family to maintain their lifestyle in the event of your passing. For the business, it ensures funds are available for a smooth succession plan or to buy out shares, keeping the business operational under your chosen leadership plan.

Disability Insurance

Disability insurance is equally crucial. As a business owner, if you were to become disabled, this coverage would replace a portion of your lost income, helping maintain both your personal finances and business operations. It ensures that even in the face of unexpected health issues, you and your business can continue to meet financial obligations. Disability insurance can also be used in buy-sell agreements, triggering a buyout if you or a partner become disabled.

Long-Term Care (LTC) Insurance

Long-term care insurance addresses the costs of long-term care services, whether in-home care, assisted living, or nursing home care. This type of insurance is particularly important as you age, helping protect your retirement savings from the high costs of long-term care services, which might otherwise deplete your financial resources.

Property and Casualty (P/C) Insurance

P/C insurance covers the physical assets of your business from risks like fire, theft, and natural disasters. It’s essential for protecting the tangible investments in your business. On the personal side, P/C insurance ensures that your home, vehicles, and other personal properties are protected, helping you avoid out-of-pocket expenses due to damages or loss.

Liability Insurance

Liability insurance shields your business from financial losses resulting from lawsuits, property damage, or injuries caused to others by your business operations or personal negligence. Without proper liability coverage, a single lawsuit could have devastating financial consequences both personally and professionally.

Cybersecurity insurance

In today’s digital age, a data breach or cyberattack can cripple a business. Cybersecurity insurance provides coverage for the costs associated with responding to a data breach, including data recovery, legal fees, and notification to affected customers.

Tailoring Insurance for your Financial Plan

Each of these insurance types serves a unique and vital role in a comprehensive insurance strategy. Together, they create a safety net that protects against the financial shocks that can occur due to health issues, disability, or even death. Additionally, these coverages support the continuation of your business’s legacy and protect your family’s financial security.

Incorporating a well-rounded insurance plan into your overall financial strategy is not just prudent; it’s a necessity that ensures continuity and security for both your personal and business spheres. As you plan for the future, consider consulting with an independent insurance specialist who understands the specific needs of business owners to tailor a plan that fits your unique circumstances.

Estate and Legacy Planning for Business Owners

Estate planning for business owners goes beyond simply naming beneficiaries. Integrating business ownership into your personal estate planning ensures that your assets, including your business interests, are distributed according to your wishes and that your business continues to thrive after your departure.

Estate planning requires considering how to support your loved ones financially after your passing, while also ensuring the smooth continuation of your business. This involves outlining who inherits your business interest, who takes over management responsibilities, and the key personnel necessary for ongoing success. Careful planning protects your legacy and ensures your wishes are carried out, both for your family and your business. Below, are specific examples of estate planning tools for business owners and how they are incorporated into a financial plan:

- Trusts: Offers advantages such as avoiding probate and providing a level of control over assets held within the trust, even after your death. Also, trusts allows giving detailed instructions for managing and distributing your business assets. Trusts, can provide significant tax benefits including helping to minimize estate taxes. A trust can be used to hold your business interest and distribute ownership to your children when they reach a certain age or gain the necessary experience. You can also set terms within the trust that outline how the business should be managed until then.

- Gifting: Provides opportunities to gift shares of the business to family member(s) in a tax-advantaged way, especially if you are considering a family transition plan. You can gradually transfer ownership of your business by gifting small shares each year. This reduces your estate value and allows family members to gain experience running the company.

- Powers of Attorney/Healthcare directives: These documents ensure someone you trust can make important financial and health related decisions on your behalf if you become incapacitated. This can be particularly important for business owners, as quick decision making can be crucial to continued business operations.

- Life insurance: Provides the liquidity needed to pay estate taxes and support business continuity plans. A properly funded life insurance plan ensures that your heirs have the financial means to maintain or transition the business according to your wishes without the need to liquidate other assets. A life insurance policy can provide your heirs with the cash they need to pay estate taxes on your business without having to sell any portion of the company.

Integrating business ownership into your estate planning requires a comprehensive approach that includes wills, trusts, powers of attorney, and life insurance. This integration not only protects your personal and business assets but also helps ensure that your legacy is maintained as you envision. Consulting with an estate planner who specializes in business ownership is advisable to tailor a plan that aligns with your personal and business goals.

Tax Planning for the Business Owner

Effective tax planning is vital for business owners, who often face more complex tax situations than regular employees. Early planning allows business owners to make decisions that could reduce their tax liability now and at the time of sale.

Optimizing Personal and Business Tax Obligations

Personal financial planning for business owners must incorporate sophisticated tax strategies that optimize both personal and business tax obligations. This includes:

- Choosing the Right Business Structure: Selecting the appropriate business entity (e.g., sole proprietorship, partnership, LLC, S-corporation, C-corporation) can have significant tax implications. The right structure can minimize taxes and maximize deductions.

- Leveraging Business Deductions: Taking advantage of all available business deductions, such as those for office expenses, travel, and employee benefits, can lower taxable income. Staying informed about changes in tax laws ensures that you capitalize on new deductions and credits.

- Smart Timing Decisions: Timing the recognition of income and expenses can impact your tax liability. For instance, deferring income to a lower tax year or accelerating expenses to a higher tax year can be beneficial.

Differences in Tax Planning

Unlike typical employees, whose tax considerations are often straightforward, business owners must navigate a more complex landscape, including:

- Pass-Through Taxation: Understanding how income flows through to personal tax returns in pass-through entities like S-corporations and partnerships.

- Self-Employment Taxes: Planning for self-employment taxes, which cover Social Security and Medicare, is crucial as these can significantly impact overall tax liability.

- Dual Roles: Business owners often act as both employer and employee, complicating payroll taxes and retirement contributions.

Understanding Tax Impact of Selling a Business

Even if it’s not an immediate concern, understanding the tax implications of selling your business is crucial for long-term planning. The sale of a business can trigger various tax consequences, including capital gains tax, depreciation recapture, and potential state taxes. Planning ahead can help structure the sale to minimize these taxes, potentially through installment sales, like-kind exchanges, or other tax deferral strategies.

By integrating these strategies into your personal financial plan, you can effectively manage and reduce your tax liabilities, ensuring that you retain more of your hard-earned money and secure a stronger financial future.

Corporate Retirement Plans

Retirement Preparedness

Unlike employees who may have employer-sponsored retirement plans, business owners are responsible for their own retirement planning. Starting early allows them to explore various retirement savings options, such as IRAs or expanding to a cash balance plan or a corporate retirement plan, such as a 401k, for the business. These options allow business owners to consistently save over a long period of time, they are not overly reliant on selling their business as their sole retirement plan.

While securing your financial future is paramount, your financial well-being extends beyond just yourself. Effective corporate retirement and executive benefit plans are crucial for attracting and retaining top talent. Regularly evaluating your existing plans ensures they remain optimal for both you and your employees.

Benefits of Corporate Retirement Plans

Diversifying Your Wealth and Building Security: One of the significant advantages of corporate retirement plans is the ability to take chips off the table. These plans allow you to contribute pre-tax dollars towards your own retirement within the plan. This effectively diversifies your net worth beyond the value of your business. Building assets outside of the company itself provides peace of mind and strengthens your long-term financial security. You’re not solely reliant on the success of your business for a comfortable retirement.

Working with Freedom Financial

Financial planning for business owners is complex. Your business is likely a major source of your wealth, but it’s also tied up in the company’s value. This makes traditional financial planning strategies less applicable.

At Freedom Financial Partners, we understand the unique challenges business owners face. We can help you develop a personalized financial plan that considers all aspects of your life, including:

- The Freedom Score: This metric helps you determine the financial target you need to achieve in order to live your desired lifestyle after leaving your business.

- Business Valuation: Knowing the true value of your business is essential. An accurate valuation empowers you to make informed decisions about your future.

- Investment Planning: We’ll help you develop an investment strategy that aligns with your goals and risk tolerance, considering the fact that a significant portion of your wealth may already be tied up in your business.

- Risk Management: We’ll help you identify and mitigate potential risks to your financial security.

- Business and Personal Insurance: We’ll help you put in place the right insurance coverage to protect yourself, your family, and your business.

- Estate Planning: We’ll help you ensure your legacy is protected and your assets are distributed according to your wishes.

- Tax Planning: Business owners face complex tax situations. We’ll help you develop strategies to minimize your tax liability.

- Retirement Planning: Unlike many employees, you likely don’t have a traditional employer-sponsored retirement plan. We’ll help you explore various retirement savings options to ensure a secure future.

- Corporate Retirement Plans: We can also advise you on setting up retirement plans for your employees, which can help you attract and retain top talent.

By working with financial planning professionals who specialize in working with business owners, you can gain the clarity and confidence you need to achieve your financial goals. We’ll partner with you to create a roadmap to your Freedom Score and help you live the life you envision, both during and after your ownership years.

If you’re ready to speak with one of our advisors, please schedule an initial consultation by emailing us at info@ffpforme.com.

Take the Quiz: Business Owner Planning Questionnaire

See how ready you are for transitions like selling your business or retiring. Discover your Financial Preparedness Score by answering 20 key questions. This assessment is a stepping stone meant to give you a snapshot of where you are today and what changes to make before you exit your business. Request your free copy today.

See how ready you are for transitions like selling your business or retiring. Discover your Financial Preparedness Score by answering 20 key questions. This assessment is a stepping stone meant to give you a snapshot of where you are today and what changes to make before you exit your business. Request your free copy today.